Apply

Apply

e-APPLY

e-SANCTION

e-DISBURSE

Start your eHome Loans Process Now!

Apply Online

Click to calculate the amount

you need to pay as your Property Loan EMI

More than

4 lakh propertiesto choose across all cities

Calculate your home loan eligibility based on your income details,

home loan tenure and home loan interest rate

You Grow, We Grow! Join us in fulfilling dreams and making people own a home of their own!

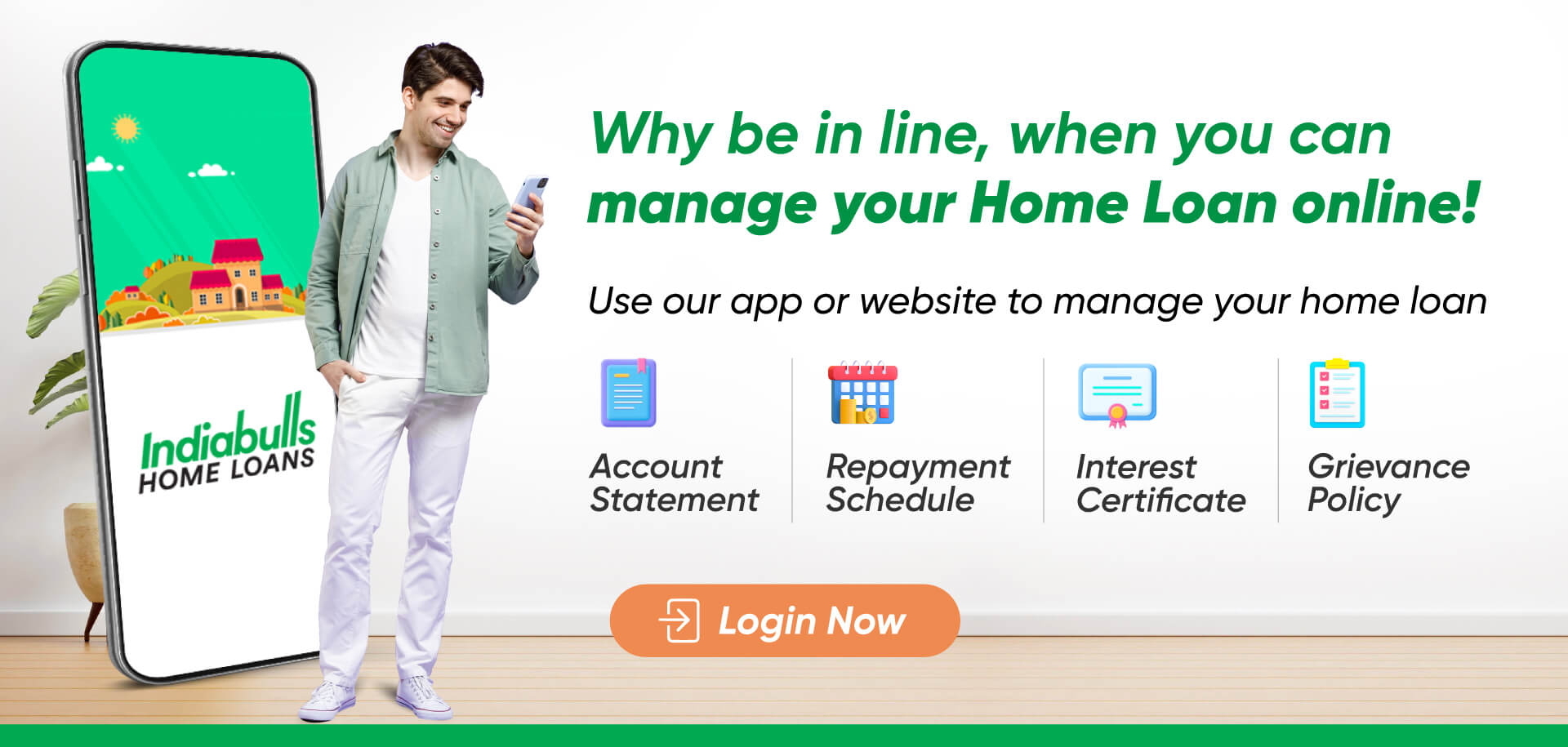

Know MoreManage your Home Loan online and with ease after disbursal

Login to your account and track your application status

Login to Your AccountMore than

4 lakh propertiesto choose across all cities

Your own home brings feelings like no other. The joy of belonging, beginning your own story, and building memories in a place that you can call your 'own' is special. We, at Indiabulls Home Loans, are committed to providing the most convenient home loan at the most attractive interest rate. We ensure utmost convenience in your home buying experience. We provide tailor-made home loan solutions to the customers to help them realize the dream of owning a home. Come; celebrate the joy of belonging to your OWN home.

Get in touch with our customer care executives.

Monday to Saturday – 9 am to 6 pm.

Except 2nd and 3rd Saturdays and Public Holidays.

Place a request for Home Loan EMI Moratorium/Deferment.